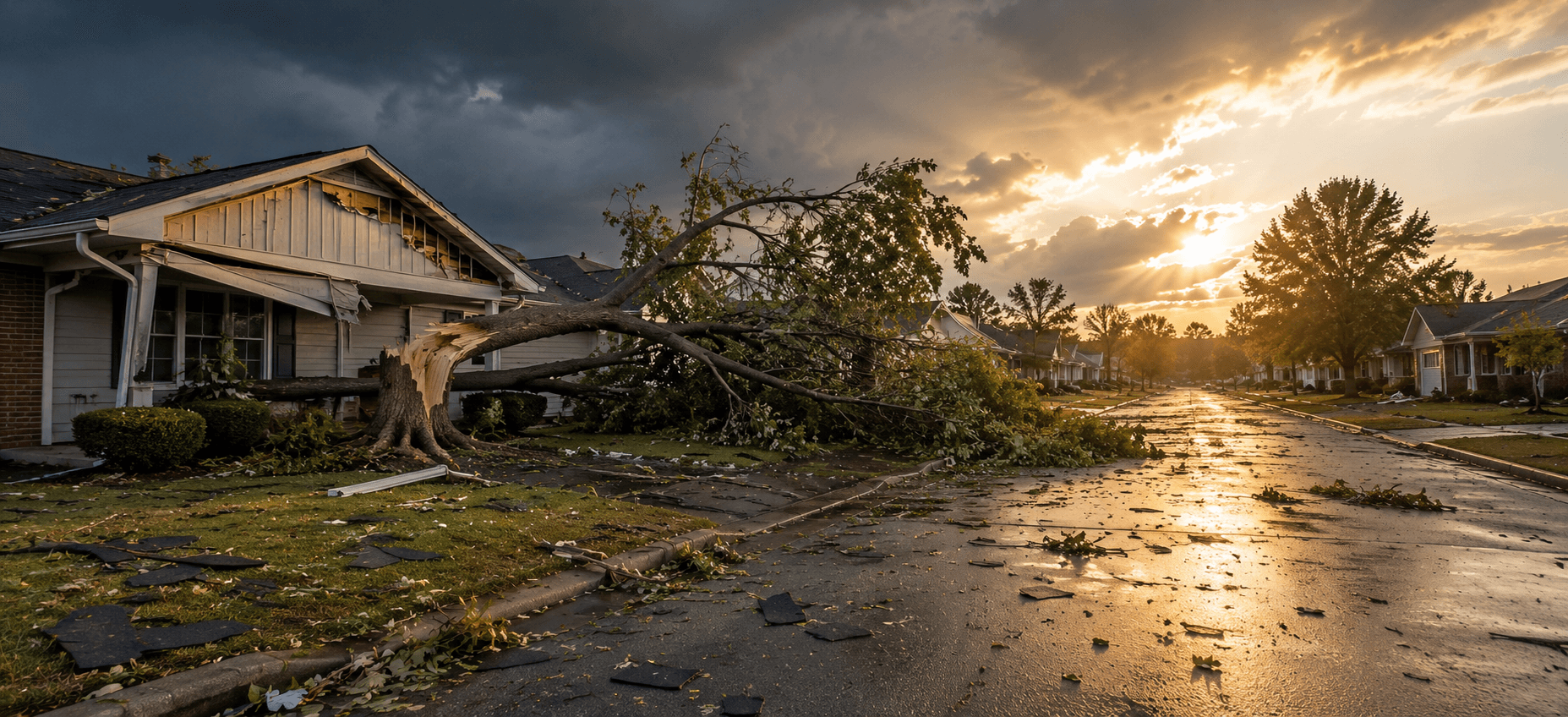

The Homeowner's Tornado Claim Playbook

What insurance doesn't explain — from total loss valuation through 18-month rebuild management. The complete 7-part guide to navigating a tornado damage claim.

The Homeowner's Tornado Claim Playbook

Tornado claims are different from almost every other homeowners insurance claim in one fundamental way: the fight is almost never about whether you're covered. A tornado clearly happened. The damage is obvious. Coverage usually isn't in dispute.

What is in dispute — sometimes quietly, sometimes loudly — is how much your home and belongings are worth, how long your insurer will pay for your housing while you rebuild, and whether the scope of what's being replaced actually matches what was destroyed.

These disputes typically take 12 to 18 months to resolve. The homeowners who come out of that process with fair outcomes aren't the ones who pushed hardest — they're the ones who stayed organized longest.

Why Tornado Claims Go Long

The biggest financial risk in a tornado claim isn't a denied claim. It's a claim that closes before the full scope is understood, or an ALE limit that runs out before your rebuild is done.

Rebuilds after major tornado damage routinely take 12 to 18 months. Permitting delays of 4-8 weeks are normal after major events. Material lead times for windows and structural components extend to 12-16 weeks in a post-disaster market. Each supplement cycle — documentation, submission, review, approval — adds time. And through all of it, a single claim generates hundreds of communications, documents, and financial records that become impossible to navigate without structure.

Organization over time is the skill that matters most in a tornado claim. Not expertise. Not aggression. Staying organized and specific across 12-18 months.

What Your Insurer Is Watching For

Scope accuracy. The adjuster's initial estimate is written for visible, verifiable damage at the time of inspection. Tornado damage is rarely contained — water intrusion from a compromised roof reaches ceilings, walls, and floors; structural shifting affects areas that look untouched from the outside. Adjusters expect supplemental claims and evaluate whether each supplement is supported by specific documentation connecting the additional damage to the covered event.

ALE reasonableness. Adjusters evaluate whether ALE expenses are reasonable given household size, pre-loss living standard, and what comparable housing actually costs in the post-disaster market. They also note whether you're managing ALE strategically — a furnished rental with a kitchen stretches coverage; a hotel at the same nightly rate doesn't.

Settlement timing. Insurers have financial incentive to close claims. A homeowner who accepts a settlement before the full scope is known and before the rebuild is documented has fewer options for what comes next. Adjusters are aware of the information asymmetry — you don't know what you don't know yet about the scope. Your protection is staying in active claim status until the rebuild is actually complete.

The First Hours: Documentation Under Impossible Conditions

You don't need to be systematic in the first hour. You need to get something. Imperfect documentation done immediately is worth far more than thorough documentation done two days later when cleanup has begun and the physical evidence has changed.

Safety before documentation. Do not enter a structurally compromised building. Once it's safe: start documenting from outside. Wide shots of every side of the exterior. Aerial documentation if anyone nearby has a drone — tornado damage seen from above tells a story that ground-level photos can't.

Document the full picture: exterior from every angle, roof from every safe vantage, interior room by room, open closets and cabinets (contents coverage depends on documenting what was there), the debris field, any neighboring structures showing the storm path.

Call your insurer within 24 hours. Start a written log from minute one — when you called, who you spoke with, what was said, what the next step is. This log will matter more than you expect as the claim stretches across months.

ALE starts now. If your home is uninhabitable — and tornado damage often makes it so immediately — every receipt from tonight forward is a potential reimbursement. Hotel, meals, laundry, storage. Log them as you go; reconstructing ALE expenses from memory weeks later is harder than capturing them in real time.

Total Loss vs. Partial Loss: The Determination That Changes Everything

The most consequential early determination in a tornado claim is whether your home is a total loss or a partial loss. This shapes how the claim is valued, how long it takes, and what decisions you face in the coming months.

Total loss doesn't require your home to be reduced to rubble. Most states define total loss as damage exceeding a threshold percentage of insured value — commonly 50-75%. A home that's structurally standing but has 60% of its value destroyed may be declared a total loss under state law.

Under a total loss, three things commonly make the insurer's offer lower than expected:

Underinsurance. If your Coverage A limit hasn't kept pace with construction cost increases, your insured value may be significantly below the actual cost to rebuild today. Construction costs have increased dramatically in recent years. Many homeowners are underinsured by 20-30% without knowing it.

Land value exclusion. Coverage A insures the structure, not the land. If your home's market value is $450,000 but $80,000 of that is land, your Coverage A may be $370,000. This is correct — but it surprises many homeowners.

ACV vs RCV. If your policy covers the structure at actual cash value rather than replacement cost, depreciation is applied. On an older home, this can represent a significant reduction.

Before accepting a total loss settlement, get an independent general contractor estimate for the full rebuild cost. If the insurer's number is significantly below that, the gap is the starting point for a supplement or appraisal process.

Partial loss tornado claims almost always require supplemental estimates as the full scope becomes clear. Every instance of additional damage found during the rebuild should be photographed, included in a contractor change order, and submitted as a supplement before the additional work is authorized.

Matching rights apply here at scale. A tornado that destroys one side of a home's siding may trigger matching rights for the entire exterior. If partial replacement would create a visible mismatch, raise matching rights in writing with your adjuster and document that you did.

ALE: Making Coverage Last Through a Long Rebuild

For tornado claims, ALE is often the most financially stressful element of the entire claim. Rebuilds routinely take 12-18 months. Many homeowners exhaust ALE before their home is ready.

ALE covers the increase in your living costs caused by displacement — the difference between what you normally spend and what you're spending now. Most policies express ALE as a dollar limit (often 20-30% of Coverage A) and a time limit (typically 12-24 months). You hit whichever comes first.

On a $400,000 Coverage A policy with 20% ALE coverage, that's $80,000 total — roughly $4,400 per month over 18 months. In a post-disaster rental market where prices have spiked and comparable housing is scarce, that gets tight quickly.

A furnished rental with a kitchen will almost always stretch ALE further than extended hotel stays at the same nightly rate. Track cumulative spending monthly against both your dollar limit and your time limit. If the rebuild timeline extends, document the delay in writing and request a formal ALE extension with your contractor's timeline as support.

If ALE exhaustion is approaching with no end in sight: get a written timeline from your contractor, request an extension formally in writing, escalate to a supervisor if your standard contact isn't responsive. Document the home's uninhabitable condition with photos and contractor statements — so the extension request is grounded in evidence, not just a request.

Coverage Gaps That Surprise Total Loss Homeowners

Ordinance or law coverage — the most commonly missing endorsement in a total loss. A home destroyed in 2026 must be rebuilt to 2026 building codes. Updated electrical systems, structural requirements, energy efficiency standards, egress requirements. The cost difference between rebuilding to original specifications and current code can be $30,000-$80,000 or more.

Most standard homeowners policies do not cover this gap. Ordinance and law coverage is a separate endorsement. Check your policy. If it's absent, raise the code upgrade costs with your adjuster with specific contractor documentation — and add the endorsement at your next renewal.

Debris removal sublimits. Removing tornado debris is expensive. A single large tree through a roof can cost $5,000-$15,000 to remove. Multiple trees plus structural demolition debris can easily exceed $30,000-$50,000. Most policies include debris removal coverage but with a sublimit — often 5% of the total claim. On a $300,000 claim, that's $15,000. Know your sublimit and get a specific written estimate for debris removal as a separate line item before work begins.

Contents at scale. In a total loss, you're replacing the entire contents of a home. The total value is almost always higher than homeowners estimate — and without a prior home inventory, you're reconstructing from memory. Start room by room, category by category. Use credit card and bank statements to reconstruct major purchases. Check your phone's photo history and social media — images taken inside your home before the loss document what was there.

State-Specific Notes

Oklahoma and Kansas sit in the highest-frequency tornado corridor in the country. Standard HO-3 policies are the norm, and most tornado claims involve straightforward wind coverage with no flood complication. The main issues are scope disputes, contractor availability post-event, and ALE exhaustion on long rebuilds. Oklahoma Insurance Department at oid.ok.gov; Kansas Insurance Department at ksinsurance.org.

Texas sees significant tornado activity in addition to hail. In some coastal areas, wind coverage may come from TWIA rather than a standard homeowners insurer — know which entity covers your wind damage. Prompt payment under Tex. Ins. Code §§542.055–.058 (Prompt Payment of Claims Act) — acknowledge within 15 days (§542.055), accept/reject within 15 business days of receiving the items required for proof of loss (§542.056), pay within 5 business days of acceptance (§542.057). Verified as of 2026-07-20; confirm current law. Complaints at tdi.texas.gov.

Alabama, Mississippi, and Tennessee — Dixie Alley — produce significant tornado events with older housing stock and substantial ordinance/law exposure. Pre-1990s homes in this region face the largest gap between original construction standards and current code. Verify whether your policy has ordinance or law coverage before a loss.

All states. Acknowledgment and decision timelines vary by state — look up your state's rule rather than relying on a general range. When these timelines are exceeded, a formal complaint to your state insurance commissioner creates a record the insurer must respond to within a defined timeframe.

Frequently Asked Questions

My home was declared a total loss. Can I negotiate the settlement amount? Yes — and you should before signing anything. Get an independent general contractor estimate for the full rebuild cost. If it exceeds the insurer's offer, submit it with a written supplement request. If negotiations stall, invoke the appraisal clause — most policies allow either party to demand binding appraisal of the value of a covered loss. This is the appropriate mechanism for exactly this type of dispute.

What is the appraisal clause and when should I use it? The appraisal clause is a provision in most homeowners policies allowing either party to demand a formal valuation process when there's a genuine disagreement on the dollar value of a covered loss. Each party selects an independent appraiser; if they can't agree, a neutral umpire decides. It's not litigation — it's a standard policy mechanism. Use it when supplement negotiations have stalled after two or three rounds and the gap is material. Check your policy's Conditions section for the demand deadline, which is sometimes time-limited after receiving the insurer's estimate.

My ALE limit is going to run out before my home is rebuilt. What are my options? Formally request an extension from your insurer in writing, with your contractor's timeline as supporting documentation and a clear explanation of what's causing the delay. Escalate to a supervisor if your standard contact isn't responsive. Document the home's uninhabitable condition with photos and contractor statements. The strongest extension arguments are those where the delay is caused by factors outside your control — permitting, material availability, or insurer-caused delays in supplement approvals.

Do I have to use my insurer's preferred contractors? No — you can choose your own licensed contractor. Verify their license through your state's contractor board, get multiple written estimates, and confirm they have experience with insurance rebuild projects. Be cautious of contractors who offer to "handle your insurance claim" — this is an AOB situation. Your insurer may push toward preferred vendors; you are not required to use them.

How do I handle the contents claim on a total loss? Start room by room, systematically. Use every available record: credit card and bank statements for major purchases, retailer account order histories, email receipts, phone photos, social media images showing your home's interior. Don't filter yourself at the inventory stage — include everything you remember and let the documentation determine what gets paid. Contents value is almost always higher than initial estimates.

What if my adjuster keeps changing throughout the claim? Every time an adjuster changes, send a written status summary to the new adjuster within a week: approved supplements, open items, ALE status, pending decisions, and prior commitments. A claim that spans 18 months may see two or three different adjusters — the homeowner with a complete written record of what was committed to is in a fundamentally different position than one relying on memory.

Most tornado claim disputes resolve in favor of organized homeowners — not because they fought harder, but because they knew more precisely what they were owed and could demonstrate it clearly. Organization over time is the real skill. ClaimEase tracks every communication, every document, and every ALE expense in one place — so nothing gets missed across the months it takes to get your life back.

ClaimEase provides general guidance. Coverage determinations are made by your insurer based on your specific policy terms. Consult a licensed public adjuster or insurance attorney for specific advice about your claim. State laws and policy terms vary.