The Homeowner's Hurricane Claim Playbook

The two-policy reality, wind vs. flood determination, and what two claims actually look like. The complete 8-part guide to navigating a hurricane damage claim.

The Homeowner's Hurricane Claim Playbook

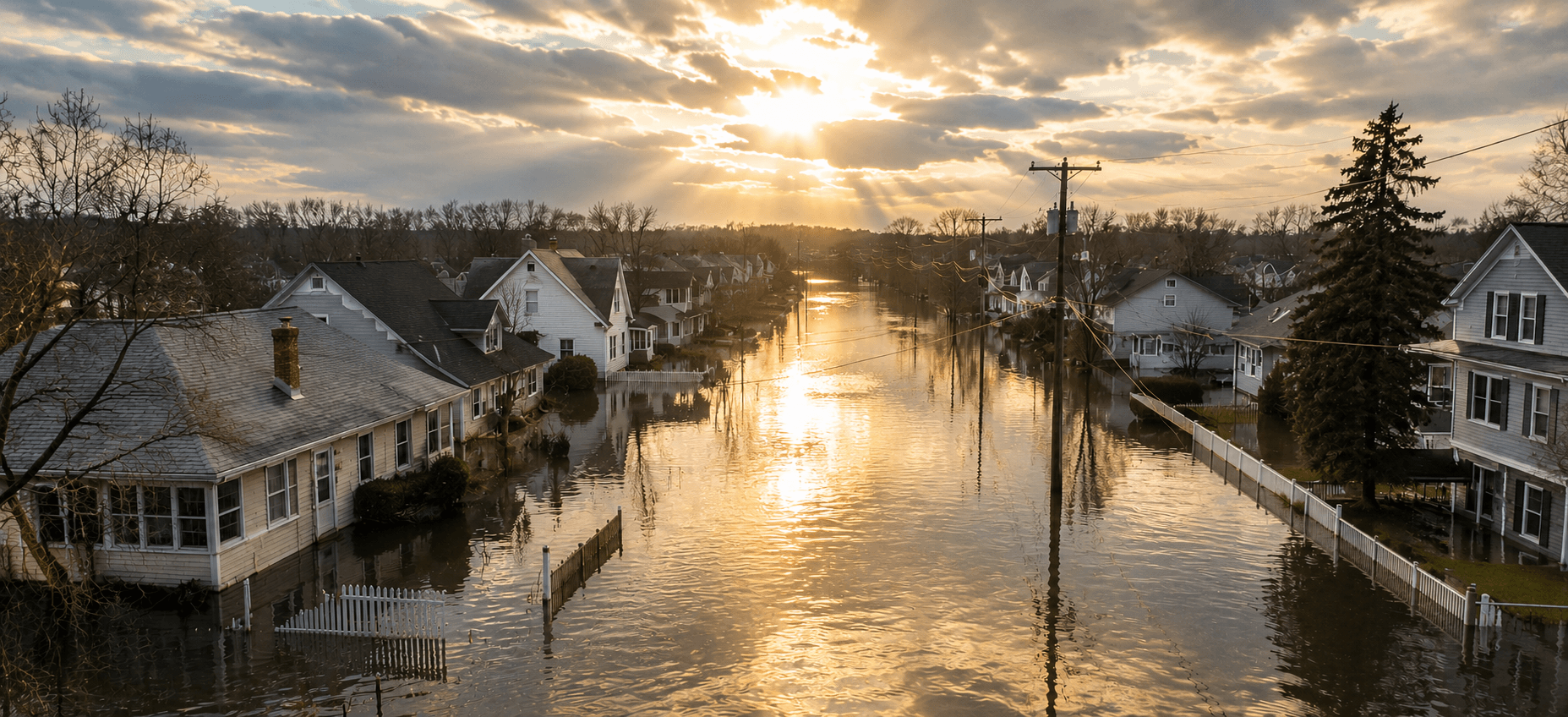

Most homeowners going into hurricane season believe they have one insurance company, one claim, and one check coming if their home is damaged. The reality is more complicated — and the gap between that assumption and the truth is where most hurricane claim money is quietly lost.

A hurricane brings two perils: wind and flooding. Those two perils are covered by two completely separate policies, administered by two separate adjusters, on two separate timelines. Your homeowners policy covers wind. A flood policy covers flooding. If you don't have a separate flood policy, flood damage is not covered at all.

This matters because your homeowners insurer has a financial incentive to attribute as much damage as possible to flooding — the peril they don't cover. The homeowners who navigate hurricane claims successfully understand this dynamic before it happens to them.

Why Hurricane Claims Are Different From Every Other Claim Type

The defining feature of a hurricane claim is the wind/flood split. Almost every other major loss type involves one peril, one policy, one adjuster. A hurricane involves two of each — and the boundary between them is exactly where disputes concentrate.

This split exists because flooding is excluded from standard homeowners policies. Flood coverage comes only from a separate policy — through the National Flood Insurance Program (NFIP) or a private flood insurer. The NFIP has its own structure, its own limits ($250,000 for structure, $100,000 for contents), its own adjuster, and critically its own rules: NFIP contents are covered at actual cash value only — no replacement cost — and NFIP provides no Additional Living Expense coverage at all. If your home is uninhabitable due to flooding, your flood policy pays nothing toward temporary housing.

Understanding this two-policy reality before a storm determines whether you can actually make yourself whole after one.

What Your Insurer Is Watching For

Two things drive most hurricane claim disputes.

The wind/flood attribution question. Your homeowners insurer is motivated to attribute damage to flooding. Your flood insurer is motivated to attribute damage to wind. The homeowner caught between two insurers who each attribute damage to the other can end up undercompensated by both. Adjusters make this determination based on where water entered (above through a wind breach, or from below as rising water), the water line relative to the exterior flood level, and the sequence of events.

The mold clock. In coastal climates, visible mold can appear within 24-48 hours of water intrusion. Most homeowners policies include mold coverage but sub-limit it — typically $10,000-$25,000. If an insurer can demonstrate that mold resulted from unreasonable delay in mitigation, they may contest remediation costs entirely. "Did the homeowner take reasonable steps to mitigate immediately?" is a question every hurricane adjuster asks.

Before the Storm: The Decisions That Actually Matter

Unlike hail or tornado, hurricane preparation has a meaningful lead time. Once a storm is named and approaching your coastline, most insurers stop writing new policies and stop making coverage changes. What you have at that point is what you have.

Named storm deductibles — know the dollar amount. Most coastal homeowners policies include a separate deductible specifically for named storm or hurricane damage — almost always expressed as a percentage of Coverage A, not a flat dollar amount.

A 5% named storm deductible on a $500,000 home means $25,000 out of your pocket before insurance pays anything. On a $750,000 home, that's $37,500. These numbers are large enough to affect whether filing makes sense for moderate damage. Check your declarations page and calculate the dollar amount against your current Coverage A limit.

Flood insurance — and when you can't get it. NFIP policies have a mandatory 30-day waiting period before coverage takes effect. A flood policy purchased after a storm is named provides no coverage for that storm. If you're in a coastal or flood-prone area without flood insurance, the time to buy it is before storm season — not when you see a storm on the map.

Pre-season documentation. A thorough video walkthrough before storm season establishes the pre-storm condition of your home (protecting you from pre-existing damage disputes) and documents your contents (establishing your personal property baseline). Do this annually. Store it somewhere that survives the same storm that damages the home — cloud storage, a secure email account.

Know which company covers what. In Texas coastal counties, wind coverage often comes from the Texas Windstorm Insurance Association (TWIA) rather than a standard homeowners insurer. In Florida, Citizens Property Insurance is the state-backed insurer of last resort. Many other coastal states have similar wind pools. Know which entity covers your wind damage before you need to file a claim with them.

The First 72 Hours: Two Claims, Two Clocks

Safety before documentation. Do not enter a structurally compromised building. Do not walk through standing floodwater — it may carry electrical hazards, contamination, or structural damage hidden below the surface.

Document with the coverage question in mind. Every photo you take should capture information that determines which policy pays. Photograph the high-water mark on exterior and interior walls — flood evidence. Photograph roof damage, window breaches, and siding failures — wind evidence. For every area of interior water damage: did water come from above through a wind-created opening, or from below as rising water? Document the answer visually.

Document the sequence if possible. If you sheltered in place, note what you observed and when — when wind damage occurred, when water began rising. Written notes with timestamps created at the time carry significantly more weight than recollections written weeks later.

Begin mitigation immediately. Tarp roof openings. Start drying saturated materials. Get a licensed water mitigation company to your property within 48 hours if at all possible. Emergency mitigation is required by your policy, reimbursable, and the only thing that holds the mold clock. Do not wait for adjuster inspection to begin drying — waiting is failing to mitigate, and that has consequences.

Call both insurers the same day. Your homeowners insurer and your flood insurer. Both have prompt notice requirements. Two policies, two claim numbers, two communication logs starting now.

The Wind vs. Flood Determination

The wind/flood determination is the central dispute in major hurricane claims. Understanding how adjusters make this call — and how to document your position — is what separates homeowners who recover fully from those who don't.

Adjusters make the determination based on: where water entered (above through a wind breach or below as rising water), the water line position relative to exterior flood levels, and the sequence of events. Wind damage typically affects upper portions of structures; flood damage affects lower portions. Interior water damage on your second floor is more consistent with wind-driven rain through a breach than with flooding.

If either insurer attributes damage to the other policy, request a written explanation citing the specific evidence for that determination. A verbal attribution is the opening position in a negotiation — not a final answer. The wind/flood split is an interpretation of evidence. Homeowners who document thoroughly and push back on unsupported attributions reach better outcomes than those who accept the first determination without question.

Managing Two Claims Simultaneously

Do not wait for one claim to settle before pursuing the other. Pursue both aggressively and independently. Payment timelines will differ — one claim may settle in 60 days while the other takes 6 months. Track both separately.

NFIP-specific rules: Structure coverage caps at $250,000 — if your home's rebuild value exceeds that, the gap requires an excess flood policy or is out of pocket. Contents are ACV only — a five-year-old $4,000 television may be valued at $800-$1,000. There is no ALE coverage under NFIP.

File your NFIP Proof of Loss within 60 days of the loss if you intend to dispute any aspect of the flood settlement. Missing this deadline can forfeit your right to challenge the determination under the federal process.

The most dangerous financial position in a hurricane claim is when both insurers attribute significant damage to the other policy — and the two offers together don't cover actual repair cost. Documenting both adjusters' positions in writing, from both inspections, creates the record you need to address this gap specifically.

State-Specific Notes

Texas. Wind coverage in coastal counties often comes from TWIA rather than a standard homeowners insurer. TWIA has its own adjuster network, claim timelines, and dispute process. Named storm deductibles in coastal Texas are commonly 2-5% of Coverage A. Complaints at tdi.texas.gov.

Florida. Citizens Property Insurance covers hundreds of thousands of coastal homes. Hurricane deductibles commonly range from 2-5% of Coverage A, with higher deductibles in some coastal zones. Florida has significant AOB restrictions (Fla. Stat. §627.7152, the 2019 assignment-of-benefits reform, HB 7065) — know your rights before signing anything. Complaints at myfloridacfo.com. Verified as of 2026-07-20; confirm current law.

Louisiana. Louisiana Citizens covers homes where private market coverage is unavailable. Named storm deductibles are common. Complaints at ldi.la.gov.

All coastal states. Acknowledgment and decision timelines are set by state regulation and vary — look up your state's rule, and note that state wind pools may operate under their own claim procedures. File regulatory complaints when timelines are exceeded.

Frequently Asked Questions

I have homeowners insurance but not flood insurance. Is any flood damage covered? No — flooding is explicitly excluded from standard homeowners policies. If you don't have a separate flood policy, flood damage is not covered, period. If your home has both wind and flood damage, only the wind damage goes to your homeowners insurer.

What is the 30-day NFIP waiting period? NFIP policies have a mandatory 30-day waiting period before coverage takes effect — meaning you cannot buy a flood policy when a storm is approaching and have coverage for that storm. There are limited exceptions but they don't apply to most situations. The time to buy flood insurance is before storm season.

Both my homeowners and flood adjusters are attributing damage to each other's policy. What do I do? Document both positions in writing from the start. Request written explanations from each insurer citing the specific evidence for their causation determination. Then present both written positions together with your documentation — sequence notes, photos showing damage patterns at different levels — in a formal dispute submission. A public adjuster experienced in hurricane claims is most valuable in exactly this scenario.

When does ALE start and what does NFIP cover for temporary housing? ALE under your homeowners policy starts when your home is uninhabitable due to wind damage. NFIP has no ALE provision at all. If flooding is the sole or primary cause of uninhabitability, your homeowners ALE coverage may be contested. Keep every displacement expense receipt from the first night.

How long do hurricane claims typically take? Simple wind claims can resolve in 4-8 weeks. Claims involving both wind and flood, scope disputes, or NFIP involvement routinely run 6-18 months. Major regional events extend timelines across the industry — adjuster assignment can take 4-6 weeks after a large storm. Filing promptly and pursuing both claims simultaneously keeps both moving.

Do I need a public adjuster for a hurricane claim? More often than for other claim types. The two-policy complexity, the wind/flood determination dispute, and the volume of supplemental damage common in hurricane claims all create situations where a licensed public adjuster's experience recovers more than their fee. For claims over $75,000 or any claim where both insurers are attributing damage to the other policy, the calculation almost always favors representation.

Managing a hurricane claim well doesn't require expertise in insurance law. It requires understanding the two-policy reality before the storm, documenting the wind/flood split from the first hour, pursuing both claims simultaneously, and staying organized across what is often a 6-18 month process. ClaimEase tracks both claims in one place — so when one insurer attributes damage to the other policy, you have the record to respond specifically rather than from memory.

ClaimEase provides general guidance. Coverage determinations are made by your insurer based on your specific policy terms. Consult a licensed public adjuster or insurance attorney for specific advice about your claim. NFIP policies are subject to federal regulations that may differ from state law.